Energy security- a primarily theoretical concept in recent years that has been made startlingly real by the recent developments in Ukraine. But what could the possible repercussions of this crisis be on European energy policies and our fuel bills?

I had a chance to ask this question during a recent event at the House of Commons, hosted by the APPCCG and Sandbag. The answer surprised me.

According to Baroness Worthington, director of Sandbag and member of the House of Lords, two outcomes are broadly possible.

|

| Figure 1: Map of Ukraine |

If Ukraine `turns on the taps’, this would solve their immediate energy dependence on Russia and produce a revenue stream to support their economy. However, exploiting natural resources on the scale required would require significant investment, and Ukrainians would have to accept the change in land use and economic transformations that come with becoming a major energy exporter.

This optimistic outcome seems open to several criticisms. It’s unclear at this moment where investment would come from, and whether Russia would oppose competition in the European energy market. Moreover, can Ukraine ever completely replace Russia as an energy supplier? For instance, Russia’s natural gas reserves are around 40 times the size of Ukraine’s.

The second scenario is of a destabilised Ukraine, whose policies are influenced to a significant degree by Moscow. In this situation, European nations would need to purchase natural gas in the short-to-medium term from Russia and Ukraine, and tamely accept price rises and the uncertainty and energy insecurity that comes with dependence on a foreign nation for energy supplies.

This second possibility may also be criticised; Russia may not have further demands after the annexation of Crimea is completed. It may be the case that Russia wish to return to business as usual as quickly as possible, and may choose to offer energy supplies on favourable terms to Europe in order to encourage the resumption of trade and renewed trust.

In my view, both scenarios will result in one predominant outcome: the loss of trust. It seems unlikely that Russia can regain the trust of the West quickly; by it’s very nature, trust takes years to accrue and moments to lose. Energy security will become a much larger talking point in the next few years if relations with Russia continue to remain cool. Nations that previously were willing to base their energy supply on foreign gas purchases will choose instead to pay a price or environmental premium to source those supplies from more trusted sources.

The nations most likely to make changes to their energy mix as a result of this crisis are Germany and Poland. Germany’s choice to abandon nuclear fission after the Fukushima crisis leaves them slightly more vulnerable to a loss of fuel supplies from abroad, and they may choose to shift further towards renewables, or attempt the politically difficult U-turn of returning to nuclear power. Poland uses natural gas and coal to power much of its economy, a significant portion of which is purchased from Russia. Since the fall of the Soviet Union, Poland has been consistently suspicious of Russia, and may decide that now is the time to reduce or remove their dependence on Russian supplies.

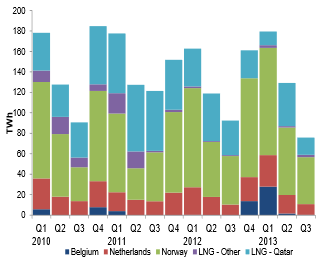

|

| Figure 2: DECC figure for natural gas supplies by source, 2010-2013 |

Perhaps the Ukraine crisis will be the public relations coup the shale gas industry has been looking for.

|

| Neeraj Oak |