How can the Government best retain key skills and re-skill and up-skill the UK workforce to support the recovery and sustainable growth?

This summer the UK’s Department for Business, Energy and Industrial Strategy (BEIS) requested submission of inputs on Post-Pandemic Economic Growth. The below thoughts were submitted to the BEIS inquiry as part of input under the EnergyREV project.

However, there are points raised here that, in the editing and summing up process of the submission, were cut out, hence, this blog on how the UK could power economic recovery through Smart Local Energy Systems (SLES).

1. Introduction: Factors, principles, and implications

In order to transition to a sustainable and flourishing economy from our (post-)COVID reality, we must acknowledge and address the factors that shape the current economic conditions. I suggest to state the impact of such factors through a set of driving principles for the UK’s post-COVID strategy. These factors are briefly explained below along with suggested principles that acknowledge and account for these factors:

1. Zero-carbon economy targets: Given the zero-carbon economy targets for 2050, one could clearly see that any investment other than that in carbon-neutral or carbon-reducing assets will either jeopardise the set targets, or lead to stranding these assets within the next 30 years. As a result, we suggest Principle 1: focus the UK’s investments on green and renewables-based initiatives.

2. Energy is the engine of the economy: It is therefore essential to both grow and expand the clean energy system so that the economy, as a whole, flourishes. This leads us to Principle 2: special focus on supporting greening of the energy system is of prime importance.

3. Localisation trend: Evidently, localisation is emerging as a strong trend due to a number of diverse reasons, such as:

- Health: continuous threat of the spread of the COVID-19 virus. The restricted mobility between variously affected localities is likely to be expected, at least, within the medium term, as local outbreaks occur and are contained [1];

- Technology: most renewable energy technologies are dependent on the availability of locally distributed renewable sources. For instance, tidal energy can only be harvested on the shore side, while sufficient solar generation can be expected from localities with sunny weather, etc.

- Local governance: local communities have a stronger sense of their identity and many prefer to work together (locally) in order to address the challenges they face.

- Resilient architectures: distributed, decentralised organisations (be it for critical and non-critical infrastructure, businesses, community, etc.) are much more resilient when faced by threats (e.g., from floods to disease outbreaks).

Thus, we suggest Principle 3: the UK should aim for a locally distributed systems architecture across all areas of infrastructure, business, and society.

4. Smart, globally inter-connected ecosystem: While distributed and decentralised assets are most resilient to systemic failures, they also must be monitored, coordinated and interconnected if they are to act as a single economic and social ecosystem and not just as a set of disjointed assets. Thus, we suggest Principle 4: Smart technology must underpin the distributed, de-centralised economy and ecosystems for monitoring, access, coordination, control and communication.

The UK has already taken the first steps towards smart local energy systems (SLES) through a programme of research and development embodied in 4 large-scale demonstrators (The Energy Superhub Oxford, ReFLEX Orkney, Project Leo, Smart Hub SLES), several design projects and numerous pilots [19]. And, more than that, many innovative businesses (such as Verv and Electron) and non-for profit organisations (such as Community Energy England, Centre for Sustainable Energy) and local/regional authorities (such as Bristol and Manchester City Councils) are well underway in implementing much of the above in practice. Yet, these activities must be systematically replicated while contextually adapted to each locality, and radically scaled up.

As stated by P. Devine-Wright [2], “Local Energy involves professional organisations, primarily partnerships between public and private sectors, with a focus upon public authorities taking a coordinating role to leverage private sector investment in local energy provision.” Here, the local energy landscape is defined to include a range of energy related activities [3]: generating energy; reducing energy use through energy efficiency and behaviour change; managing energy by balancing supply and demand; and purchasing energy.

All of this draws on a range of skills: organisation, communication, management, governance, regulation, technical and technological, business innovation and so on.

The smart aspect of energy system often implies digitally supported coordination of decision-making for a system to optimise its resource use and waste reduction (both generation and consumption), fault tolerance and recovery from failures, support for human decision-making for efficiency and comfort. All of this draws on the skills of software, hardware, and power system engineers [4]. Thus, a particular attention needs to be paid to the “smart” technology occupations and skills training.

On the other hand, the smart energy system will not fulfil its potential without smart users, thus the household and business users also need to acquire skills in the functioning and use of digital energy systems [5–8].

The above noted principles have many implications, a few of which we note below:

1. If clean and renewables-based economy is to take off (as driven by principles 1 and 2) there is a need for a long-term cross-party commitment to investment into and development of such energy systems. There is ample evidence that uncertain, unpredictable, and changeable policy on renewable energy leads to dis-investment and skills loss in these sectors.

2. If distributed architectures are to be successful across the UK’s economy, local authorities would require more financial independence and regulatory support, as well as more accountability for fostering grass-root innovation and participation in the energy sector and economic transition.

3. If smart technology is to underpin the transition, a wide variety of training and educational programmes need to be delivered (from on-the-job training to mass educational programmes through media and specialised university degrees) to enable country-wide participation and contribution. The various areas of skills development are discussed further in section 2.

1.1. On Green Jobs

It is also worth noting that the first two suggested principles necessitate both transition to renewables-based technologies and to green jobs. Currently there are a number of definitions of what a ‘green job’ is [9–11]. To state briefly, it appears that any job has the potential of becoming a green or greener job by changing the practices of the company or service/product lifecycle, as long as it will reduce the environmental impact of enterprises and economic sectors, ultimately to levels that are sustainable [11].

However, this does not offer any means to statistically distinguish between green and non-green jobs [11]. Should a green job be defined by the level of emissions involved or the purpose of the job [12]? Moreover, the standard data concerning employment and the labour market structure does not account for any definition of green jobs either.

Nevertheless, some work has focused on defining profiles of ‘green jobs’ and observing if such jobs differ from non-green ones in terms of skill content and of human capital. For instance, [13] notes that green jobs require more interpersonal skills and require more formal education, work experience and on-the-job training.

Yet other research notes that many of the green jobs that will be in demand as a result of a transition to a low carbon economy are not new jobs as such. Rather, the transition will see a shift of workers in conventional energy industries such as engineers and installers, to apply their expertise in the low-carbon sector [14].

Thus, on green jobs, we observe that:

1. Transition to SLES with green jobs not only has the potential to support the economy to flourish, but will also lead to a more skilled and better qualified workforce within the UK overall.

2. In order to support this transition (and to monitor and coordinate the job market, as per principle 4) clear definition of and operationalisation for statistical data collection on green jobs is needed.

2. Areas of Skills Development

The transition to smart local energy systems has the capacity to create jobs across a number of areas within the UK economy:

2.1 Energy System

With respect to job creation, the renewables-based smart local energy systems are a workforce intensive. They require workforce for the manufacture, distribution, sale, installation, operation, and maintenance of the wide variety of locally distributed generation resources. For instance, to outfit a dwelling with PV panels, panel manufacturers and retailers must be present, installers must be available, as well as maintenance operators for the post-installation period. Additionally, various energy service providers (such as demand-side management, peer to peer trading and storage service operations) can create new businesses, working with the installed distributed generation resources. A similar set of activities is required for integration of all other renewable energy sources, from wind, bio-gas, tidal, wave, anaerobic digestion, to hydrogen. Finally, a set of aggregation and grid regulation service providers must step in to ensure that the renewables-powered localities remain reliably supplied by electricity, irrespective of the generation intermittency and are seamlessly integrated with the UK electricity grid at large and comply with the grid regulations.

Furthermore, we underline that the transition to smart local energy systems is not limited to the electricity generation and use, but must integrate heating and cooling and transportation areas.

2.2 Transportation

To support transition of transportation, the vehicle stock within the country must be re-fitted to either electric sources (electric vehicles: EVs) or to bio-gas or hydrogen fuels. This, in turn, will require new charging and re-fuelling infrastructure installation across the UK’s motorways and cities, as well as workforce to operate these. While the current workforce in refuelling stations can be re-trained to operate the new charging/re-fuelling stations through on-the-job training, the vehicle maintenance workforce will require substantial re-training as EV maintenance is dramatically different from that of present conventional fossil-powered vehicles.

2.3 Heating and Cooling

Similar to renewables-based generation sources for electricity, the transition of heating and cooling systems requires installation of new technology (such as air and ground heat pumps, bore holes, sun-powered hot water tanks, waste heat recycling). This, too, has to be supported by manufacturing, installation and maintenance professionals. Many, such as gas boiler installers, must be re-trained to new skills, e.g., heat pump installation. Some will be attracted from other domains, e.g., builders to carry out the bore hole construction. Yet others will be required to train as engineers.

2.4 Building and Retrofit

Transition to the new energy sources will require integration of such sources into the fabric of the UK’s built environment. This implies both training and regulation for the new built, and retrofit of the existing building stock. This too is a large and labour-intensive transition area, as the workforce must be trained to work in accordance with zero-carbon construction practices.

Similarly, a large-scale retrofit activity is required, e.g., to undertake energy audits, draft proofing advice provision, external and internal wall insulation. Recent experience with provision of funding for retrofit with no skilled parties to deliver it has demonstrated that poor quality workmanship and poor reputation of the scheme can cause more damage than help to further the causes of energy efficiency. Thus, measures (such as register of qualified retrofit providers, contract award only upon qualification confirmation, post-installation quality assurance/audit) must be taken to ensure that retrofit work is undertaken by qualified professionals, for which quality assurance processes and monitoring bodies need to be put in place as well.

2.5 Regulation and Governance

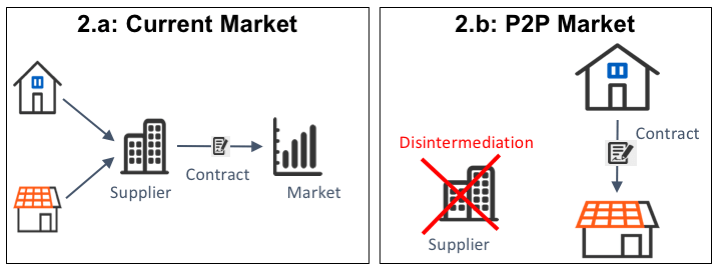

The energy sector is highly regulated and will remain so in the future due to both technical requirements (e.g., maintaining grid frequency) and critically of its continuous availability (e.g., for operation of other businesses and welfare of population). Yet, transition to SLES will require substantial regulatory review and adaptation. For instance, to enable small-scale generation and trading across household and non-energy businesses, the consumers should be able to change suppliers (as they will be often buying from their peers) very frequently (e.g., every 30 minutes) [15].

In addition, new governance structures will be necessary, e.g., a governing body to ensure consistent data collection and standard formats of data sharing across industries.

2.6 Teaching and Training

As noted before, the green jobs will require more interpersonal skills, as well as formal education, particularly in all areas of engineering as well as professionals able to work across disciplines [16]. On-the-job training [13], and re-skilling for the workforce that shifts from the conventional to the low-carbon sector [14] will also be needed alongside mass education of the population at large for using smart energy systems and services. Thus, new education and re-training programmes will be required.

Moreover, many of those currently employed in the energy or related sectors (e.g., building and transport) cannot afford to take time off for additional education and training (e.g., due to financial pressures) [17] and so on-the-job, or paid-for training delivery modes are necessary.

2.7 Impact on Supply Chains

We must also note that the supply chains of the noted areas will, in turn, be changed and re-invigorated: from manufacturing and delivery of new hardware for renewable technology, to research and development investments across the affected sectors and their suppliers.

3. Skills Needed

As discussed above, the transition to SLES requires a wide ranging workforce, with many requiring re-skilling or up-skilling. Below we provide an overview of the preliminary set of skills which are expected to be in short supply in the near future. These skills have been noted as particularly relevant by a set of current energy system practitioners [16, 17], which, though are not definitive for the UK, can be considered sufficiently representative and indicative:

1. Soft Skills, i.e., skills that are necessary for engaging with stakeholders, such as negotiating, building partnerships, organisational skills, listening and communication, time management, etc.

2. Technical Skills, i.e., sills required to install, set up, operate, and maintain the hardware and software necessary (e.g., installation and operation of heat pumps, or EV charging stations, maintenance of wind turbines and data analysis for optimisation of distributed generation and consumption, etc.).

3. Project Management Skills, such as carrying out feasibility studies, handling procurement, identification and coordination of multiple stakeholders, risk management, etc.

4. Financial Skills relate to the skills to finance or obtain funding for projects, such as accounting, fundraising, financial modelling, putting new business models together.

5. Legal skills, such as navigating the regulatory framework, assessing planning permission, managing contracts, challenging smart energy system policy.

6. Skills for Building and Retrofit, such as building carbon neutral dwellings, draft-proofing and laying insulation, inside and outside wall insulation, etc.

7. Policy Making Skills, i.e., setting out policies with insight into their short- and long-term impact, and possible ramifications on other directly and indirectly related activities within the energy sector. This requires understanding of the current state, processes and trajectories within the energy systems, as well as continuous engagement with the sector.

8. Skills for Population at Large which include, to name a few, confidence to engage with smart technology for automaton, control and optimisation of own appliances, understanding of own behavioural impact on energy system and the wider eco-system and so ability to choose the best considered behaviour in a given situation (e.g., with whom to share data or allow access to devices, etc.), ability to engage with energy efficiency measures and benefit from local renewable generation programmes and businesses, etc.

4. Avenues for Skills Acquisition

How can the Government best retain key skills and re-skill and up-skill the UK workforce to support the recovery and sustainable

4.1 Skills Retention

The recent Global Talent Index Report (GETI) [18] carried out by 17,000 respondents from 162 countries has shown that although there is an obvious skills shortage, the most worrying issue for the renewable energy sector is, in fact, the political landscape. A lack of subsidies is of huge concern to the renewable industry, significantly more so than to the conventional and better established non-renewable sectors.

However, the skills shortage is a looming crisis that many are also worried about: 60% of respondents believe there is only 5 years to act before it hits. So what talent is lacking? The discipline of Engineering was reported to be in highest need (50%) and project leadership following with 25%. The latter reinforced by the lack of understanding of the system as a whole: how multiple energy generation methods can work together and complement each other, the role of legal experts and policy makers in steering the path to change, the implementation of effective and relevant training and education programmes and how all of these factors come together.

The key risks to the sector, as a result of talent shortages, include decreased efficiency, loss of business and reduced productivity. These consequences will trigger a negative feedback loop since it is likely that there will be less incentive to work in the renewable energy industry if it is a failing one.

The top three methods to attract the right talent, agreed amongst hiring managers and professionals, include:

- Better training: Currently training provided at the universities is often considered too theoretical, and new graduates seem to lack practical experience [17], thus more practical, hands-on training is desirable.

- Clearer career progression will help the employees envision their long-term placement with this sector. Yet, clear pathways for progression are still missing.

- Increased remuneration and benefits packages are expected to make the jobs more attractive.

However, remuneration was one of the least common reasons for choosing to work in this sector. A possible explanation could be that the majority of the workforce in the renewable industry are between the ages of 25-34. The concern for the climate is more apparent among the younger employees who may enter the sector as they wish to take action against global warming rather than for gaining “job perks” [16].

4.2 Re-Skilling: cross-sector mobility

As noted in section 3 above, many of the skills necessary for enabling transition to SLES are generic, e.g., available within project managers or other workers across other domains. This is an indicator that the workforce currently employed (or recently made redundant) in other areas of economic activity could move to respective positions within the SLES domain. In order to enable such cross-sector mobility (which is relevant for retaining the skilled workforce in employment in the post-COVID environment and throughout the rapid transition to SLES), it is necessary to:

1. make information about the job profiles in SLES widely available across other sectors where adequately qualified staff may be in access of the current sectoral needs (e.g., air travel, retail, hospitality). This will ensure that those outside of SLES sector who may not have looked at SLES as a viable area of work, become aware of the open opportunities;

2. provide demonstrative cases of career transition. The cases of transition should be publicised for each sector specifically, e.g., a case whereby a manager working in airline industry has transitioned to SLES for the airline industry; a case where a store manager from retail industry is transitioning to SLES project management can be publicised within retail industry, etc. This will ensure that each sector worker can envision that those like her can transition to the SLES area. To reinforce the message that the given person has the right skill set for a particular area of SLES, the employers of those who are made redundant could be encouraged to provide this information directly to them;

3. provide opportunities for engagement, e.g., through “open days” whereby all potentially interested parties could visit a SLES workplace and/or have a (video/phone) chat with someone in a similar position of responsibility. This will help the potential applicants to envision the new sector and job to which they would be suited.

Opportunities for re-skilling and career progression/review are already available within many trade unions as part of mid-career review. We suggest that the trade unions could also be drawn upon in supporting the transition to new careers within the SLES sector.

4.3 Up-Skilling the Workforce

The need for training and up-skilling the workforce is clear, both currently in the energy sector and that newly transitioning into it (e.g., due to rapid evolution and change within the technologies, standards, and customer expectations).

However, much of the workforce will be unable to re-enter full time education or training with no income to sustain themselves and their families. As a result, those currently employed in the energy sector (as per our ongoing study) have strong preferences for:

- Shorter training courses which can be undertaken e.g., on a one or two leave day basis;

- Locally available training that is accessible in close proximity to the home/workplace;

- Paid training opportunities which will not lead to loss of earnings, as this dis-incentivises those in need of training (e.g., the builders are reluctant to take time off to qualify for zero-carbon construction if they have sufficient work in the current building industry);

- Recognition of ‘learning by doing’ or workplace training;

- Training through apprenticeships which provides the necessary practical experience along with theory content. This method of training is particularly well regarded by much of the industry.

4.4 Skills for the New Normal

We must also consider the skills necessary for the new normal work. Given that the impact of COVID will continue to unfold for, at least, the medium time, and that the UK economy must be prepared for potential other future pandemics, we suggest that particular attention should be paid to providing training for the workforce to be able to work remotely/from home, focusing on such skills as, for instance:

- digital technology literacy;

- self-organisation and time management;

- self-care and mental health;

- use of online collaboration tools and techniques.

References

[1] LeicestershireLive. Live updates: Pressure on government over lockdown release, door-to-door testing. https://www.leicestermercury.co.uk/news/leicester-news/lockdown-data-map-latest-updates- 4297621, 2020.

[2] P. Devine-Wright. Community versus local energy in a context of climate emergency. Nat Energy, 4:894–896, 2019.

[3] DECC. Community energy strategy. https://www.gov.uk/government/publications/community- energy-strategy, 2015.

[4] West of England joint committee. https://westofengland-ca.moderngov.co.uk/documents/s891/ 13, 2019.

[5] Christopher J Brown and Nils Markusson. The responses of older adults to smart energy monitors. Energy policy, 130:218–226, 2019.

[6] Denise J. Wilkins, Ruzanna Chitchyan, and Mark Levine. Peer-to-peer energy markets: Understanding the values of collective and community trading. In Proceedings of the 2020 CHI Conference on Hu- man Factors in Computing Systems, CHI ’20, page 1–14, New York, NY, USA, 2020. Association for Computing Machinery.

[7] Caroline Bird and Ruzanna Chitchyan. Towards requirements for a demand side response energy management system for households. arXiv preprint arXiv:1908.02617, 2019.

[8] Ruzanna Chitchyan and Caroline Bird. Theory as a source of software requirements. In Proceedings of the 28th International Requirements Engineering Conference, RE’2020. IEEE, 2020.

[9] Gabriela Miranda, Hyoung-Woo Chung, David Gibbs, Richard Howard, and Lisa Rustico. Climate Change, Employment and Local Development in Extremadura, Spain. OECD Local Economic and Employment Development (LEED) Working Papers 2011/04, OECD Publishing, Paris, 2011.

[10] Construction Industry Training Board. Skills Needs Analysis of the Construction and Built Environment Sector in Wales Theme : Onsite and offsite construction in Wales. Technical report, CITB, 2013.

[11] Con Gregg, Olga Strietska-Ilina, and Christoph Büdke. Anticipating skill needs for green jobs: A practical guide. ILO, Geneva, 2015.

[12] Joshua Wright. Green Jobs, Part 3: Green Pathways: A data-driven approach to defining, quantifying, and harnessing the green economy, 2009.

[13] Davide Consoli, Giovanni Marin, Alberto Marzucchi, and Francesco Vona. Do green jobs differ from non-green jobs in terms of skills and human capital? Research Policy, 45(5):1046–1060, 2016.

[14] Olga Striestska-Ilina, Christine Hofmann, Durán Haro Mercedes, and Jeon Shinyoung. Skills for Green Jobs: A Global View: Synthesis Report Based on 21 Country Studies. International Labour Office, Skills and Employability Department, Job Creation and Enterprise Development Department, Geneva, 2011.

[15] Jordan Murkin, Ruzanna Chitchyan, and David Ferguson. Goal-based automation of peer-to-peer electricity trading. In From Science to Society, pages 139–151. Springer, 2018.

[16] Yael Zekaria and Ruzanna Chitchyan. Exploring future skills shortage in the transition to localised and low-carbon energy systems. 2019.

[17] Yael Zekaria and Ruzanna Chitchyan. Qualitative study of skills needs for community energy projects. In Conference on Energy Communities for Collective Self-Consumption, 2020.

[18] Airswift and Energy Job line. The Global Energy Talent Index Report 2019, 2019.

[19] Prospering from energy revolution, url: https://www.ukri.org/innovation/industrial-strategy-challenge-fund/prospering-from-the-energy-revolution/#pagecontentid-8, Accessed 20 Sept. 2020.

—————————–

This blog is written by Cabot Institute member Dr Ruzanna Chitchyan, at the University of Bristol. Ruzanna is a senior lecturer in Software Engineering and an EPSRC fellow on Living with Environmental Change. She works on software and requirements engineering for sustainability.

|

| Dr Ruzanna Chitchyan |