As part of Green Great Britain Week, supported by BEIS, we are posting a series of blogs throughout the week highlighting what work is going on at the University of Bristol’s Cabot Institute for the Environment to help provide up to date climate science, technology and solutions for government and industry. We will also be highlighting some of the big sustainability actions happening across the University and local community in order to do our part to mitigate the negative effects of global warming. Today our blog will look at ‘Technologies of the future: clean growth and innovation’.

1. Background

Today over 94% of the energy market in the UK is dominated by the Major Power Producers (MPP) who generate electricity and feed it to households and businesses over the grid [1].

Historically, to cut down on the fuel transportation costs, the major generation plants had to be located close to the fuel sources, i.e., where coal and oil were mined. The generated electricity would then be transmitted through power lines and distribution stations down to the households and businesses who would use the electricity up.

This structure of the industry was based on several constraints:

- Electricity generation locations are constrained by the location of fossil sources (as it is cheaper and easier to transmit the generated electricity than to move fuel around);

- Electricity generation requires large investments into large plants (due to economies of scale of the generation technology);

- Electricity end users are only interested in consumption, and do not want to know much else about electricity itself.

Yet, technological advances as well as the societal understanding of the implications of the fossil fuel use have dramatically changed the framework within which the energy system operates:

- Renewable generation technologies (such as solar panels, wind turbines, small hydro turbines) are now widely available for individual household and small community use.

- As (most) renewable generation resources (e.g., solar or wind) are available where consumers are, it is technologically possible and economically affordable to generate and consume electricity locally, without centralised generation and transmission;

- End users are increasingly interested in the environmental and social impact of the generated electricity, not only in consumption.

All the above, combined with the governmental subsidies for renewables installations (e.g., feed-in-tariffs) have led to a recent growth of micro-generation in the UK (i.e., individuals or organisations with small-scale energy generation, such as domestic wind or solar PV units). Such micro-generators consume their own generated energy and sell any excess back to the grid. Such generation offers the potential for a distributed model of energy generation and consumption that is not reliant on MPPs.

Challenge

Though presently, there is a successful renewables-based ecosystem in the UK, it has been largely driven by governmental subsidies. However, these subsides are now set to be withdrawn. As of March 2019 no new installations will be eligible to feed-in-tariffs. Will this result in fall of the renewables sector, as already experienced by solar PV sector in Spain [2] when their solar PV subsidies were removed? Or can UK micro-generators find another way of ensuring viability of renewable installations?

Opportunities

Research at the University of Bristol suggests that a subsidy-free localised renewables-based energy sector is not only possible but is also the best solution to the energy security and affordability dilemma. Our proposed model for the new, modernised UK energy sector is based around localised, but globally interconnected peer-to-peer energy markets underpinned by digital technology. This is illustrated in Figure 1 below:

|

| Figure 1: Peninsula peer-to-peer energy market (from [6]) |

2. Peer-to-Peer energy market underpinned by digital platform

In a peer-to-peer energy market any two individuals/households can directly buy from and sell to each other, without intermediating third parties. These households can be both prosumers (i.e., producing and consuming own renewables-based electricity, as well as selling the excess to others), on simply consumers (if they have not own generation). Yet, unlike most microgrids, this is not an islanded model – which would require complete internal balance of supply and demand – but rather a “peninsula”. Where the locality experiences shortage or excess generation, the demand/supply are imbalance is resolved through trade with the other localities or the grid at large. The key advantages here are in providing avenues for:

- Additional income streams to households with microgeneration – where the feed in tariff is no longer pays for the extra generation, the peers who use the energy do. Moreover, the price of the locally generated/consumed energy is more competitive than that of the grid supply as it does not need to pay the same full transmission, distribution, and utilities services charges. (Though I must underline that, as each locality remains interconnected with the gird, the energy costs will still include grid connection and maintenance changes. This is because the intermittency of the renewables generation must be insured against, and grid provides such an insurance and balancing services.)

- Increasing value proposition of microgeneration and energy storage – the microgenerators are not only getting return to their generation investment, but are also supporting local communities’ energy needs, contributing to the decarbonisation and energy security efforts.

- Increased control over source of supply – consumers are now able to express their preferences on energy purchase: do they wish to buy solar or wind, from the closest geographically located producer or from the cheapest supplier; do producers wish to donate their excess generation to the local school or to their extended family members, or to sell it to the highest bidder? All these options become viable when peers directly buy and sell from each other.

Such an energy system, however, cannot exist without a reliable and trusted digital platform which will both remove the 3rd party intermediation, and advertise the sale and purchase orders between the trading parties, undertake the users’ preferences-based matching of these orders, ensure security of the transitions, transparency of the trades, and accountability of the transaction participants.

To operate in such market:

- the consumers and prosumers would join the platform and publish their preferences (e.g., sell to the highest bidder, or buy solar energy only, etc.);

- the participants will they use their smart meter data to periodically (e.g., for every 15 min or half an hour) publish their sale and purchase orders on a digital platform;

- for each trading period (e.g., 15 min.) the platform will match best fitting sale and purchase orders, and settle transaction accounts.

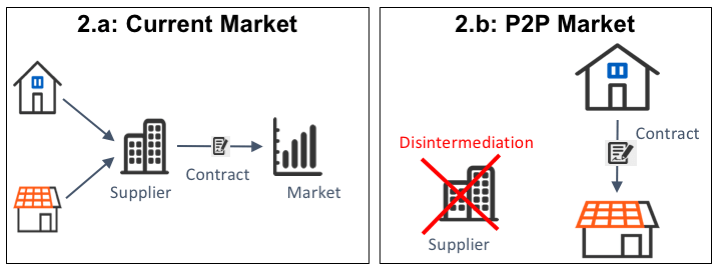

Note, (as illustrated in Fig 2) while in the current intermediated market the utilities act as the contracting parties between the prosumers, consumers and the energy market (see Fig. 2.a), in this peer-to-peer market each prosumer/consumer is the immediate contracting party itself (see Fig. 2.b).

|

| Figure 2: Energy Market Dis-intermediation (from [6]) |

To realise these demanding requirements, we advocate use of distributed ledger technology for the energy trading platform [3, 4, 7]. Distributed ledgers (which incorporate blockchain and block-free technologies) are decentralised, distributed databases in which all transactions are immutably recorded. In other words, these are databases which are not controlled by any single company or individual, but are run and maintained by their participating membership. Data in these ledgers is redundantly stored in many locations, and cryptographically secured. As a result, once recorded, the data in the ledger cannot be changed and falsified [1].

The details on how to engineer this platform in such a way that engenders trust and participation is a topic of the HoSEM research project [5] and will be detailed in another blog post. For now, let’s assume that this platform is in successful operation. What are the implication of it on the UK energy market?

3. Implications on energy market

Move to a peer-to-peer energy trading over a distributed ledger will lead to several major changes in the UK’s energy system, to name a few:

- First and foremost, it changes the structure of the energy system itself – from centralised fossil-based generation to decentralised, distributed, local renewables–based generation and consumption set up;

- The digital technology-based market disintermediation (see section 2) deprecates the role of a trusted 3rd party (utilities in this case), reducing both the cost of transactions (i.e., energy) to the end users and allowing for the best possible preferences match to each participant. Now the suppliers are switched every trading period (e.g., every 15 min.), without any effort or cost to the market participants.

- This structure also radically changes the role of the energy user – from the passive consumer to an active prosumer. The end user now matters, as every unit of produced and consumed energy is different. It is different because it is produced in the users’ local area, or is originated from solar/wined/gas sources, or is bought from a friend… Then the price of each energy unit is also different and that difference is decided on basis of the participants preferences.

Clearly, many issues remain to be resolved before this shift to a digitally enabled peer to peer market becomes a reality. These include issues of regulation and licensing (presently households are not allowed to act as suppliers in the UK), grid safety (e.g., current frequency assurance), geographical and population density (e.g., rural areas have more renewable per-person than cities), fairness and pricing (more affluent individuals can afford more generation installations), to name a few. Yet, it is encouraging to see that technologically and economically this future can be here already today.

Footnote

[1] Theoretically it is possible, but practically it is improbable, as record falsification is designed to be prohibitively costly [3].

References

[1] Dep. of Energy and Climate Change Updated energy and emissions projections 2015 Tech. Rep., URL: https://www.gov.uk/government/publications/updated-energy-and-emissions-projections-2015

[2] The rise and fall of solar energy in Spain, URL: http://www.abacoadvisers.com/spain-explained/life-in-spain/news/rise-and-fall-solar-energy-in-spain

[3] R. Chitchyan, J. Murkin, Review of Blockchain Technology and its Expectations: Case of the Energy Sector, URL: https://arxiv.org/abs/1803.03567

[4] J. Murkin, R. Chitchyan, D. Ferguson, Goal-Based Automation of Peer-to-Peer Electricity Trading, URL: https://link.springer.com/chapter/10.1007/978-3-319-65687-8_13

[5] Household-Supplier Energy Market, URL: https://gtr.ukri.org/projects?ref=EP%2FP031838%2F1

[6] Used from J. Murkin, R. Chitchyan, D. Ferguson, Towards peer-to-peer electricity trading in the UK, Presented at All Energy 2018, URL: https://reedexpo.app.box.com/s/plwhcfaqp6pnhxc8mcjznh7jtkevg9h1/file/292636529562

[7] J.Murkin, Automation of peer-to-peer electricity trading, blog post at https://www.edfenergy.com/about/energy-innovation/innovation-blog/research-development-peer-to-peer-trading

———————————-

This blog is written by Cabot Institute member Ruzanna Chitchyan from the University of Bristol Faculty of Engineering and has been reposted from Refactoring Energy Systems blog.

|

| Ruzanna Chitchyan |

Read other blogs in this Green Great Britain Week series:

1. Just the tip of the iceberg: Climate research at the Bristol Glaciology Centre

2. Monitoring greenhouse gas emissions: Now more important than ever?

3. Digital future of renewable energy

4. The new carbon economy – transforming waste into a resource

5. Systems thinking: 5 ways to be a more sustainable university

6. Local students + local communities = action on the local environment